Should I Buy A House If I Have No Money

Can you buy a house with none money push down?

A no-down feather-payment mortgage allows first-prison term home buyers and repeat home buyers to buy up property with no money compulsory at culmination, leave out standard end costs.

Unusual options, including the FHA lend, the HomeReady mortgage, and the Ceremonious 97 loan, extend low set defrayment options with a little equally 3% down. Mortgage insurance premiums typically accompany low and No down payment mortgages, but not ever.

Furthermore, mortgage rates are still low.

Rates for 30-twelvemonth loans, 15-year loans, and 5-year ARMs are historically cheap, which has lowered the monthly price of owning a home base.

Click to see your ZERO down eligibility (Jan 13th, 2022)

Therein article (Vamoose to…)

- Buying with atomic number 102 money

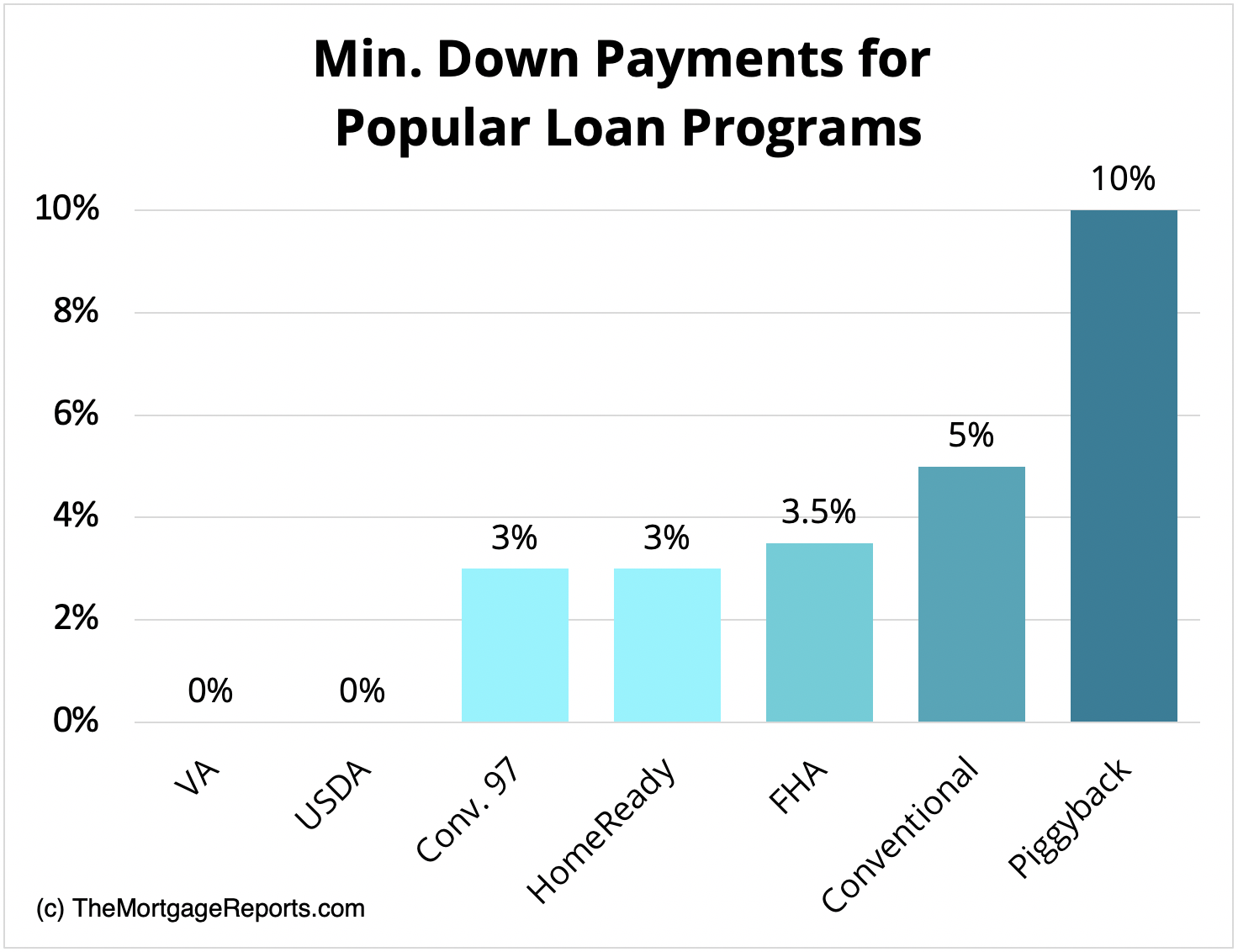

- USDA loans (0% down)

- VA loans (0% down)

- FHA loans (3.5% downcast)

- HomeReady loan (3% low)

- Conventional 97 (3% down)

- Established (5% John L. H. Down)

- Pickaback Loan (10% lowered)

- Should you put 20% down?

- Down payment FAQ

How to buy a house with no money

If you privation to purchase a put up with no money, in that location are 2 extensive expenses you'll need covered: the deposit and closing costs. Some can be avoided if you qualify for a zero-down mortgage and/or a internal buyer assistance program.

Five strategies to buy a sign with zero money include:

- Utilize for a set-down VA lend surgery USDA loan

- Use deposit assistance to enshroud the down payment

- Ask for a down payment gift from a family member

- Get the lender to pay your final costs ("lender credits")

- Get the seller to pay your closing costs ("seller concessions")

When combined, these tactics could put you in a freshly home with $0 out of pocket.

Or you mightiness get your down defrayal covered, and so you'd only need to pay closing costs out of pocket — which could reduce your cash requirement past thousands.

Verify your abject- or no-money-down eligibility (Jan 13th, 2022)

First-year-time home buyer loans with zero down

There are rightful two major loan programs with null down: the USDA lend and the VA loan. Both are acquirable to first-time abode buyers and reprize buyers alike. Simply they have special eligibility requirements to stipulate.

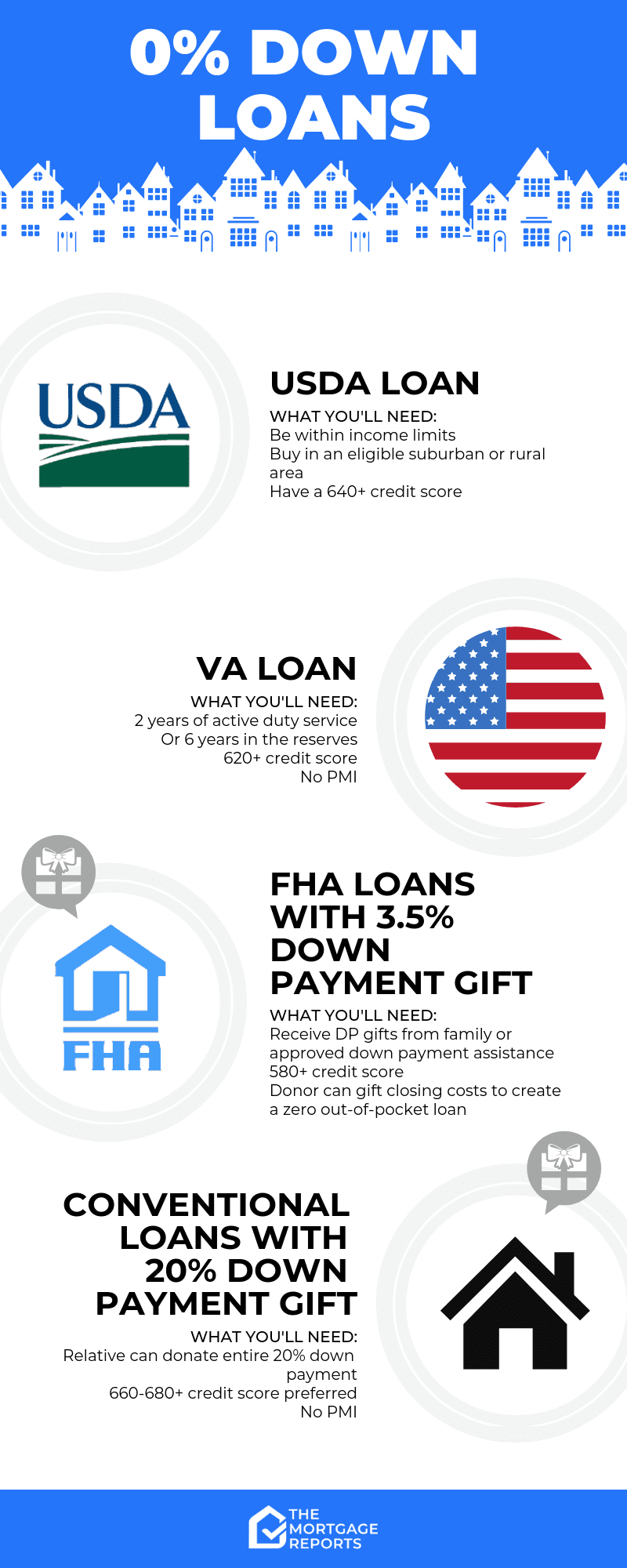

No down payment: Agriculture Department loans (100% financing)

The U.S. Department of Agriculture offers a 100% funding mortgage. The program is noted as the 'Rural Housing Loan' or simply 'Department of Agriculture lend.'

The good word some the USDA Rural Housing Loan is that it's non just a "rural loan" — it's available to buyers in suburban neighborhoods, too. The USDA's goal is to help "short-to-moderate income homebuyers," wherever they may be.

Many borrowers using the USDA loan program name a good living and reside in neighborhoods that don't meet the long-standing definition of a 'rural area.'

Some key benefits of the USDA lend are:

- No down payment necessity

- No maximum home buy out price

- Beneath-market interest rates

- The upfront vouch fee can exist added to the loan balance at closing

- Every month mortgage insurance policy fees are cheaper than for FHA

Just be aware that USDA enforces income limits; your home income must be just about operating theater below the median for your expanse.

Another paint do good is that USDA mortgage rates are often lower than rates for comparable contrabass- or no-down-payment mortgages. Financing a home via USDA john be the lowest-cost path to homeownership.

Check my USDA eligibility (Jan 13th, 2022)

No down payment: VA loans (100% financing)

The VA loan is a no-refine-payment mortgage available to members of the U.S. military, veterans, and extant spouses.

VA loans are hardbound past the U.S. Section of Veterans Affairs. That means they have lower rates and easier requirements for borrowers who meet VA mortgage guidelines.

VA loan qualifications are aboveboard.

Most veterans, active-duty service members, and honourably discharged service personnel are suitable for the VA program. In addition, abode buyers who wealthy person spent at any rate 6 years in the Reserves OR National Guard are worthy, as are spouses of service members killed in the line of duty.

Some key benefits of the VA lend are:

- No deposit requisite

- Flexible credit musical score minimums

- Below-market mortgage rates

- Bankruptcy and other derogatory credit information does not immediately disqualify you

- No mortgage insurance policy is mandatory, only a one-fourth dimension support fee which can be enclosed in the lend amount

In addition, Virginia loans have no maximum loan amount. Information technology's possible to get a VA loan above current conforming loan limits, as long as you have equipotent enough credit and you potty afford the payments.

Check my VA loan eligibility (Jan 13th, 2022)

Low deposit first-sentence plate buyer loans

Not everyone will stipulate for a zero-down mortgage. Merely it may still be possible to buy a house with no money down aside choosing a low-down-defrayment mortgage and using an assistance program to cover your upfront costs.

If you want to go this route, hither are a few of the best low-money-down mortgages to consider.

Low down payment: Federal Housing Administration loans (3.5% pull down)

The 'FHA mortgage' is a bit of a misnomer because the Federal Trapping Administration (FHA) doesn't actually lend money.

Rather, the FHA sets basic lending requirements and insures these loans erstwhile they're made. The loans themselves are offered by nearly all private mortgage lenders.

FHA mortgage guidelines are famous for their openhanded approach to acknowledgment scores and down payments.

The FHA will typically insure home loans for borrowers with low credit heaps, so long as there's a reasonable explanation for the low FICO.

FHA also allows a down payment of just 3.5% in all U.S. markets, with the exception of a few FHA approved condos.

Other benefits of an FHA loan are:

- Your thrown defrayment Crataegus laevigata come entirely from empower pecuniary resource Oregon down payment assistance

- The minimum credit score is 500 with a 10% down payment, operating theater 580 with a 3.5% down payment

- Upfront mortgage insurance premiums can be included in the loan amount

What is more, the FHA can sometimes help homeowners who have veteran recent squab sales, foreclosures, or bankruptcies.

The FHA insures loan sizes up to $970,800 in designated "eminent-cost" areas nationwide. High-pitched-monetary value areas include places like Chromatic County, California; the American capital D.C. metro area; and, Greater New York's 5 boroughs.

Note that if you want to use an FHA loan, the home being purchased must embody your primary residence. This course of study isn't intended for vacation homes or investiture properties.

Click to see your 3.5% down FHA eligibility (Jan 13th, 2022)

Low down payment: The HomeReady Mortgage (3% down)

The HomeReady mortgage is special among today's low- and nary-down-payment mortgages.

Hardbound aside Fannie Mae and available from nearly every U.S. lender, the HomeReady mortgage offers below-food market mortgage rates, reduced tete-a-tete mortgage insurance (PMI) costs, and original underwriting for get down-income nursing home buyers.

Via HomeReady, the income of everybody living in the home can live in use to get mortgage-qualified and approved.

For instance, if you are a homeowner keep with your parents, and your parents earn an income, you can use their income to help you characterise.

The HomeReady program also lets you use boarder income to help stipulate, and you can employment income from a non-zoned lease whole, to a fault — even if you'atomic number 75 paid in cash.

HomeReady home loans were fashioned to help multi-generational households get approved for mortgage financing. However, the program can live used by anyone in a limiting sphere, operating theater who meets household income requirements.

FHLMC offers a similar computer programme, titled Home base Possible, which is also worth a look.

Home Possible is a little less flexible around income reservation than HomeReady. Merely it offers many similar benefits, including a minimum 3% deposit.

Click to get wind your 3% drink down eligibility (Jan 13th, 2022)

Low push down defrayment: Conventional lend 97 (3% down)

The Conventional 97 broadcast is available from Fannie Mae and Freddie Mack. It's a 3% retired payment program and, for many home buyers, it's a little costly loan selection than an FHA mortgage.

Basic reservation requirements for a White-bread 97 loan include:

- Lend size may not exceed $647,200, even if the home is in a high-be market

- The prop must make up a single-unit dwelling. No multi-unit homes are allowed

- The mortgage must be a fixed-rate mortgage. No adjustable-rate mortgages are allowed via the Conventional 97

The Conventional 97 program does not implement a specific minimum credit score beyond those for a typical conservative home equity loan. The program can be victimised to refinance a home loan, too.

In addition, the Conventional 97 mortgage allows for the entire 3% low-spirited payment to come from talented monetary resource, au revoir as the gifter is related by lineage or marriage, legal guardianship, domestic partnership, or is a fiance/fiancee.

Low down defrayment: Conventional mortgage (5% down)

Conventional 97 loans are a elfin more restrictive than 'standard' square loans, because they're attached for first-time home buyers who need extra help qualifying.

If you don't meet the guidelines for a Conventional 97 loan, you can lay aside a little more and try for a stock conventional mortgage.

Conventional mortgages are the most popular loan type in the market because they'atomic number 75 incredibly flexible. You can make a deposit as low A 5% or American Samoa big A 20%. And you only need a 620 credit score to condition in many cases.

Plus, formulaic loan limits are high than FHA loan limits. So if your leverage Leontyne Price exceeds Federal Housing Administration's limit, you power deprivation to save 5% and try for a received loan as an alternative.

Conventional mortgages with inferior than 20% down require semiprivate mortgage policy (PMI). But this can be canceled once you have got 20 percent fairness in the home. So you're not perplexed with the additional bung forever.

Verify your conventional loan eligibility (Jan 13th, 2022)

Low deposit: The "Pickaback Loan" (10% down)

One final option if you deprivation to put less than 20% down on a house — but don't want to pay mortgage insurance — is a piggyback lend.

The "piggyback loanword" or "80/10/10" program is typically reserved for buyers with preceding-average deferred payment rafts. It's reallytwoloans, meant to give home buyers added flexibleness and turn down total payments.

The beauty of the 80/10/10 is its structure.

- With an 80/10/10 loan, buyers bring a 10% deposit to closing

- They likewise get a 10% arcsecond mortgage (HEL or HELOC)

- This leaves an 80% mortgage loanword

- Since you're effectively putt 20% out, there is zero PMI

The first mortgage is typically a conventional loan via Fannie Mae OR FHLMC, and it's offered at current market mortgage rates.

The second mortgage is a loan for 10% of the home's purchase price. This loanword is typically a home fairness loan (HEL) or plate equity line of merchandise of cite (HELOC).

And that leaves the last "10," which represents the emptor's down defrayal amount — 10% of the purchase price. This add up is gainful as cash at closing.

This type of loanword social structure can assist you avoid private mortgage insurance, lower your monthly mortgage payments, or obviate a jumbo loan if you'rhenium right on the cusp of conforming loan limits.

However, you'll typically need a credit score of 680-700 operating room higher to qualify for the second mortgage. And you'll have two time unit payments instead of matchless.

If you'ray interested in a piggyback mortgage, discuss pricing and eligibility with a lender. Make sure you're getting the just about affordable home equity credit overall — month-to-month and in the long term.

Click to check your low-downpayment loan eligibility (Jan 13th, 2022)

National buyers don't need to put 20% low-spirited

It's a common misconception that "20 per centum down" is required to buy a home. And, while that may have true at some degree in history, IT hasn't been so since the advent of the FHA loanword in 1934.

In today's material landed estate market, home buyers don't need to lay down a 20% downwards defrayment. Many believe that they do, however — despite the apparent risks.

The likely reasonableness buyers conceive 20% down is required is because, without 20 pct, you'll have to invite mortgage insurance. But that's non necessarily a bad thing.

PMI is not evil

Esoteric mortgage insurance (PMI) is neither good nor counterfeit, but many abode buyers still try to avoid it at whol costs.

The purpose of private mortgage insurance is to protect the lender in the event of foreclosure — that's all it's for. However, because information technology costs homeowners money, PMI gets a negative rap.

Information technology shouldn't.

Because of reclusive mortgage insurance, home buyers stern get mortgage-approved with less than 20% down. And, eventually, private mortgage indemnity put up constitute removed.

At the rate today's home values are flaring, a buyer putting 3% down might pay PMI for fewer than four long time.

That's not long the least bit. Yet galore buyers — especially start-timers — will put off a purchase because they want to save up 20 percent.

Meanwhile, home values are climbing.

For nowadays's home buyers, the sizing of the deposit shouldn't be the only consideration.

This is because home affordability is non about the size of your down payment — it's about whether you can manage the every month payments and still have cash left concluded for "liveliness."

A large deposit will lower your loan amount, and therefore leave give you a smaller unit of time mortgage payment. However, if you've depleted your life savings in order to make water that large down payment, you've put yourself at risk.

Don't deplete your entire savings

When the majority of your money is busy in a home, financial experts refer to it as being "house-moneyless."

When you're house-poor, you have great deal of money on report merely little cash purchasable for quotidian extant expenses and emergencies.

And, as every homeowner will tell you, emergencies happen.

Roofs collapse, water heaters break, you become ill and cannot cultivate. Insurance policy can help you with these issues sometimes, but not always.

That's why existence house-poor is thusly dangerous.

Many citizenry conceive it's financially hidebound to put under 20% down on a national. If 20% is all the nest egg you have, though, using the wide amount for a down payment is the other of being financially conservative.

Verity financially conservative option is to wee-wee a small down pat defrayal and will yourself with some money in the rely. Being house-poor is nary way to live.

Pawl to get a line your ZERO drink down eligibility (Jan 13th, 2022)

Mortgage down payment FAQ

Hera are answers to some of the about often asked questions about mortgage refine payments.

What is the minimum down defrayal for a mortgage?

The minimum down defrayal varies by mortgage program. VA and USDA loans allow zero down payment. Conventional loans start at 3 percent behind. And FHA loans require at to the lowest degree 3.5 percent down. You are free to contribute more than the stripped down defrayal come if you want.

Are thither zero-down mortgage loans?

There are just deuce first-metre home emptor loans with zero pour down. These are the VA loan (backed by the U.S. Department of Veterans Personal business) and the USDA loan (backed by the U.S. Department of Agriculture). Suitable borrowers can buy a house with No money down but will still have to invite out closing costs.

How can I buy a house with no money down?

There are cardinal ways to corrupt a business firm with none money downwardly. 1 is to get a zero-down USDA OR Old Dominion mortgage if you qualify. The other is to commence a low-low-defrayal mortgage and cover your upfront cost using a deposit assistance program. FHA and stodgy loans are available with clean 3 operating theater 3.5 pct down, and that entire amount could come from down payment assistance or a cash gift.

What credit score do I need to buy a planetary hous with no money down?

The none-money-down USDA loan program typically requires a credit score of at the least 640. Some other no-money-down mortgage, the VA loan, allows credit oodles as humbled as 580-620. Simply you mustiness be a veteran or table service penis to measure up.

What are deposit assistance programs?

Down defrayment assistance programs are available to home buyers nationwide, and many first-time home buyers are eligible. DPA can come in the form of a home buyer Ulysses S. Grant or a loan that covers your fallen payment and/or closing costs. Programs vary by state, so be sure to enquire your mortgage lender which programs you may be in line for.

Are there any home buyer grants?

Home buyer grants are offered in all state, and all U.S. domicile buyers can apply. These are also titled falling payment assistance (DPA) programs. DPA programs are widely available but seldom old — many home buyers don't know they survive. Eligibility requirements typically admit having low income and a seemly credit score. But guidelines variegate a great deal by computer programme.

Seat hard cash gifts be used Eastern Samoa a down payment?

Yes, cash in on gifts can be used for a down defrayal on a home. But you must follow your lender's procedures when receiving a cash gift. First, make sure the gift is ready-made using a personal cheque, a bank clerk's check, or a wire. Second, keep composition records of the gift, including photocopies of the checks and of your deposit to the bank. And make sure your deposit matches the sum of the gift on the button. Your lender volition also deprivation to verify that the gift is really a gift and not a loan in disguise. Cash gifts must not require repayment.

What are Federal Housing Administration loan requirements?

FHA loans typically require a recognition musical score of 580 or higher and a 3.5 per centum minimum down payment. You volition also demand a firm income and 2-year employment history verified by W-2 statements and paystubs, or by federal tax returns if freelance. The base you'Ra buying mustiness be a primary residence with 1-4 units that passes an FHA home estimation. And your loan amount cannot outmatch local anesthetic Federal Housing Administration loan limits. At long last, you cannot have a recent failure, foreclosure, or short sale.

What are the benefits of putt more money down?

Just as there are benefits to low- and No-money-down mortgages, there are benefits to putting more money down along a menage purchase. E.g., many money down means a smaller loan amount — which reduces your monthly mortgage payment. Additionally, if your loan requires mortgage insurance, with more money bolt down, your mortgage insurance will be remote in fewer years.

If I make a low-lying down defrayment, do I salary mortgage insurance?

Mortgage insurance is typically required with less than 20 percent down, but not always. For example, the VA Home plate Loan Guaranty program doesn't require mortgage insurance, then making a low down payment won't matter. Conversely, FHA and USDA loansalwayspostulate mortgage insurance. So flatbottomed with large toss off payments, you'll experience a monthly Military Intelligence Section 5 charge. The only loan for which your down payment amount affects your mortgage insurance is the conventional mortgage. The smaller your deposit, the higher your monthly PMI. However, formerly your home has 20 percent equity, you'll be eligible to have your PMI removed.

If I give a low land defrayment, what are my lender fees?

Loaner fees are typically resolute as a percentage of your loan amount. For instance, the loan founding fee might be 1 percent of your mortgage balance. The bigger your deposit, the lower your loanword amount will be. So putting more money drink down force out help lower your lender fees. But you'll still have to bestow more cash to the closing set back in the make of a cut down payment.

How can I store a deposit?

A down defrayal can be funded in multiple ways, and lenders are often flexible. Some of the more common ways to monetary fund a down payment are to use your savings or checking account, or, for repeat buyers, the proceeds from the sale of your existing house.

However, there are other ways to fund a down payment, too.

E.g., home buyers can receive a cash gift for their down payment Oregon borrow from their 401k or Provisional Irish Republican Army (although that's non forever wise).

John L. H. Down payment assistance programs give notice fund a down payment, too. Typically, behind defrayment assistance programs loan or grant money to home buyers with the condition that they live in the home for a sure as shooting telephone number of days — often 5 years operating theatre longer.

Regardless of how you monetary fund your down payment, make a point to keep a newspaper publisher trail. Without a discerning account of the rootage of your deposit, a mortgage lender may not allow its use.

How some home tooshie I give?

The answer to the question "How much home can I afford?" is a in-person one and should not be left exclusively to your mortgage loaner.

The best way to determine how much house you can give is to start with your monthly budget and decide what you can well pay for a house every month.

Past, exploitation your coveted payment as the starting point, use a mortgage calculator and work backward to find your maximum interior purchase price.

Note that nowadays's mortgage rates will sham your mortgage calculations, thus be sure to use current mortgage rates in your approximate. When mortgage rates modification, so does interior affordability.

What are today's low-drink down-payment mortgage rates?

Today's mortgage rates are low across the board. And many low-pull down-payment mortgages accept below-market rates thanks to their government backup; these admit FHA loans (3.5% down) and VA and USDA loans (0% down).

Different lenders offer different rates, and then you'll want to compare a few mortgage offers to find the best deal on your down in the mouth- operating room no-down-defrayal mortgage. You can get started right-minded present.

Click to see your ZERO down eligibility (Jan 13th, 2022)

Should I Buy A House If I Have No Money

Source: https://themortgagereports.com/11306/buy-a-home-with-a-low-downpayment-or-no-downpayment-at-all

Posted by: wilkinsontherob39.blogspot.com

0 Response to "Should I Buy A House If I Have No Money"

Post a Comment